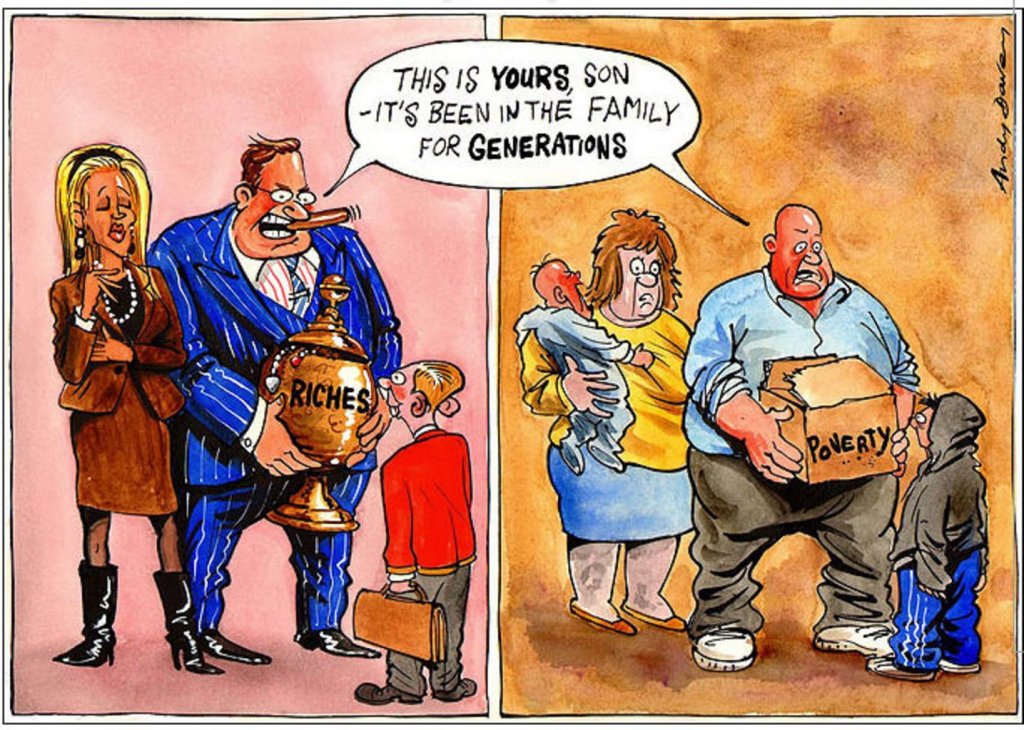

When I first started to write this post, I intended to approach it academically by defining wealth and income and highlighting the differences between the two. Then, I was going to provide data on the increasing cost of college and a declining median income. Ultimately, the point would have been that increasing college costs are contributing to inequality by impacting non-wealthy students more negatively than wealthy students.

But after consideration, I thought it might be best to tell a story. A story about a young man striving to go to college. Raised by his single mother who worked hard earning minimum wage to support her three children. Not the mother from the trashy talk shows who had three children by three different men that she “thought” were the fathers, but the mother who fell in love and had three children with the man she married. A man who lost a battle to a disease that ultimately took his life.

This family had working-class roots and there were no inheritances coming their way, or massive chunks of land that could be sold off for money. The only thing they could depend on was their own hard work to bring in enough money to meet their weekly needs. Needless to say, there were no college savings in this household. That didn’t mean that the children were not college material, it just meant quite plainly that no one in that house could afford to go. At least not without taking on a large amount of debt or first serving in one of the branches of the armed forces.

Let’s cut to the chase, I am talking about my personal experience. My choice was to join the Army. I was honorably discharged in July of 2003 and started college in the fall semester that same year. For me, what the Army enabled me to do was qualify for student loans as an independent so the burden did not fall on my mother. I also received a monthly G.I. Bill payment of around one thousand dollars for the months that I was enrolled in classes.

It sounds like a pretty good deal, and in many ways it was, but this by no means covered even the majority of my college expenses. What the GI Bill did was help pay the rent so I didn’t have to work full time while also being a full-time student. All of my tuition was covered by my student loans, and all other expenses I had to come up with on my own. My books, food, entertainment, clothes and everything else were my responsibility.

But still, what’s the problem with that? The problem occurred when it became hard to focus on school because I had to overdraft the checking account and didn’t know if I would be able to pay the rent. When I was forced to pass up the unpaid summer internship, which would have been a great experience, for the job stocking shelves at Target because eating and paying the bills was all I could afford to worry about. When I had to go the first couple of weeks in the semester without my required books before having enough money to purchase them.

The problem was after graduation interviewing for jobs, which took time and money that I didn’t really have. It meant buying a suit because I didn’t have one; it meant gas money, and in some cases staying in hotels and taking days off the job I held at the time. I had to borrow money from a friend’s dad to purchase a 1990 Toyota Corolla I needed to get job interviews from Pittsburgh to Philadelphia.

When I finally landed my first “real” job out of college, packed my car, and moved I had negative twenty dollars in my checking account. Fortunately that particular job had temporary staff housing, but unfortunately, that arrangement could only last two months. Again, what’s the problem with that?

When one starts a new job, it typically takes three to four weeks to receive the first paycheck depending on how their start date lines up with the pay period. Since I already had no money in my checking account, the first paycheck went to paying all of the bills I owed from the previous month. By that point, one month had already gone by and I still didn’t have more than a couple hundred dollars to my name. Understand that this was my first job out of college and it was in the social services field, meaning the pay wasn’t that great. So by the time I received my second paycheck, there were only two weeks for me to find a place to live.

And it wasn’t the time frame that presented the biggest challenge; it was the money. I couldn’t come up with the first month, last month and security deposit required to rent an apartment. So when my time was officially up at the staff housing, I was technically homeless. Some nights I would crash in other staff members’ rooms. One night I stayed in a hotel and even stayed in my car a couple of nights. I had purchased a membership at the Y for a place to clean up and spend some time exercising while I wasn’t at work.

This is a good place to end my story as I don’t want to diverge too far from the initial point. I was offered a room in a coworker’s home where I lived with his family for a year, and I am forever grateful to them for helping me out.

Ultimately, things have worked out OK for me, but I think it is quite easy to imagine a scenario where it wouldn’t have. And things didn’t get easier overnight. It took thirteen years from the time I graduated high school to attain some sense of financial stability, but it is going to take me even longer than that to acquire any amount of wealth. The fact remains that if I do not keep it together and continue to gain earn income and acquire some amount of wealth, my hypothetical children are destined to face the same challenges I did.

If higher education is going to continue to be a requirement for good paying jobs, we really need to start asking what extent should our earnings play a role in the educational opportunities of our children. Not only that, but we have to make sure that seeking out a college degree is going to pay off in the end. There is no backup plan for poor students. There is no nest egg to pull from if college doesn’t work out the first time around. Higher education can be the platform needed to end the cycle of poverty for a family, but it can also be the source of a crippling debt that exacerbates it.

Inequality is most likely going to be a familiar topic on my blog and I will provide more facts and statistics on the topic as I have more time to do the research. In the meantime, if you would like to read up and do some of your own research I recommend reading the following New York Times articles:

In addition, I recommend The Price of Inequality: How Today’s Divided Society Endangers Our Future by Joseph E. Stiglitz.

Leave a comment